Artificial Intelligence

Observability and Governance in RAG: Building Trustworthy AI for Insurance and Banking

A practical guide to understanding observability, governance, RAG validation, judge models, and safety guardrails—explained in simple terms for building compliant AI systems in insurance, banking, and regulated industries.

Khalid Rizvi · February 2026 · 10 min

Artificial intelligence is moving rapidly into serious business workflows—insurance claims, loan underwriting, fraud investigations, policy servicing. But once AI starts influencing decisions that affect money, coverage, or compliance, the conversation changes.

It is no longer about “Can the model generate an answer?” It becomes: “Can we trust it? Can we audit it? Can we defend it to regulators?”

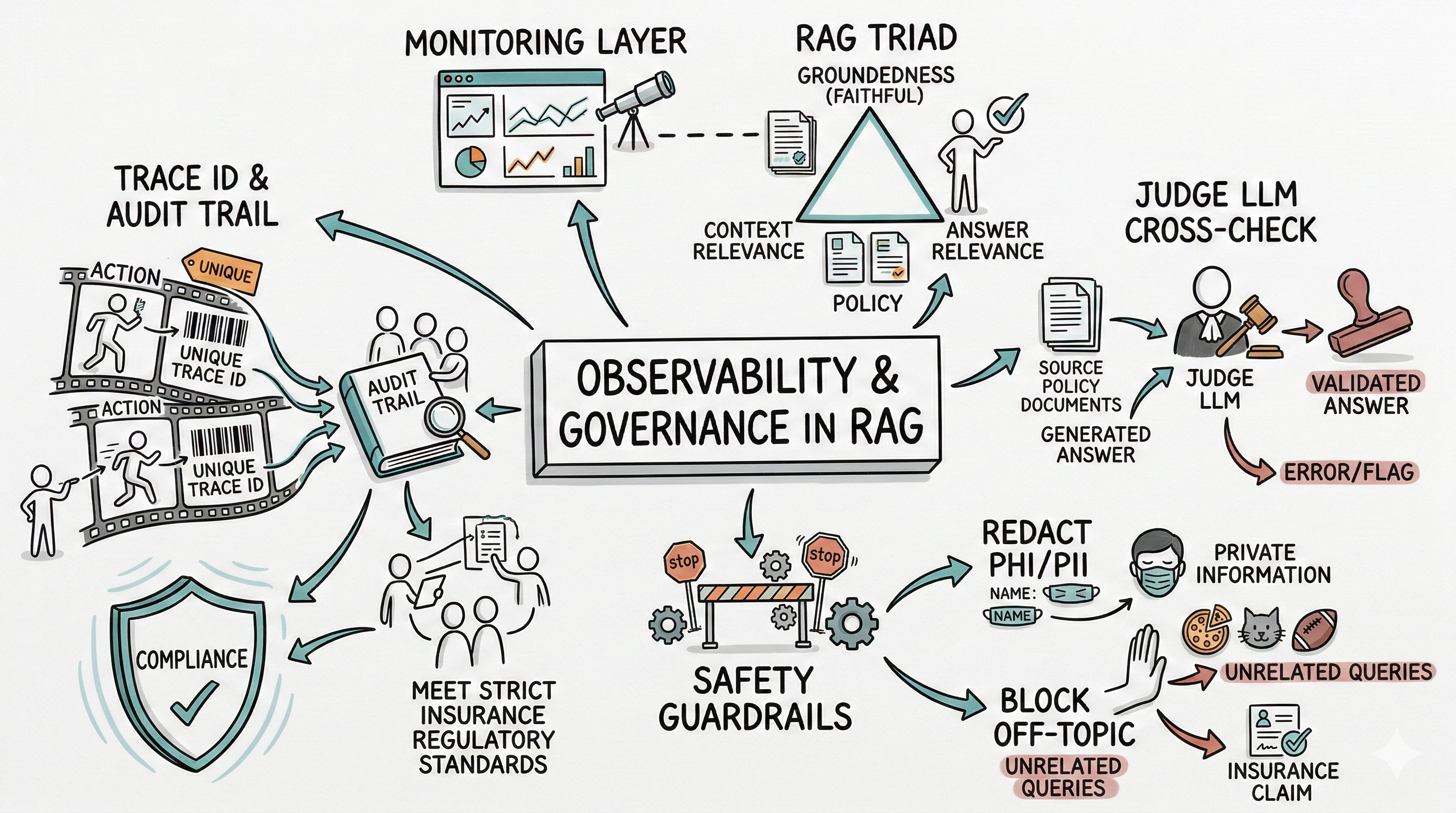

The above image is about exactly that. It explains how to make AI systems observable, governable, and safe—especially when using something called RAG, or Retrieval-Augmented Generation.

The above image is about exactly that. It explains how to make AI systems observable, governable, and safe—especially when using something called RAG, or Retrieval-Augmented Generation.

Let us walk through this slowly, concept by concept, like a professor building the foundation brick by brick.

Step 1: What Is RAG?

RAG stands for Retrieval-Augmented Generation.

A traditional large language model generates answers based only on what it learned during training. That can lead to hallucinations—answers that sound correct but are not grounded in actual data.

RAG changes this.

Instead of relying purely on training data, the system first retrieves relevant documents from trusted internal sources—policy manuals, underwriting guidelines, claim rules, regulatory documents. Only then does it generate an answer based on those retrieved documents.

Think of it like this:

Instead of asking an employee to answer from memory, you require them to look up the official handbook first and then respond.

That is RAG.

Now comes the harder part: how do we ensure that this system behaves correctly, safely, and compliantly?

That is where observability and governance enter the picture.

Step 2: What Is Observability?

Observability means the ability to see what the system is doing internally.

In traditional software, observability includes logs, metrics, and traces. If a payment fails in a banking system, engineers can trace the transaction ID and see every step the system executed.

AI systems need the same level of visibility.

When an AI generates an answer in insurance or banking, we must be able to answer questions such as:

- What documents were retrieved?

- What prompt was sent to the model?

- What version of the model was used?

- What was the generated answer?

- Were any safety rules triggered?

Without observability, AI becomes a black box.

In regulated industries, black boxes are unacceptable.

The “Trace ID & Audit Trail” in the image refers to assigning every interaction a unique identifier. That identifier allows you to reconstruct exactly what happened. If a regulator asks why a claim was denied, you can pull the trace and show the full reasoning path.

Observability is about transparency and accountability.

Step 3: What Is Governance?

Governance is about control and policy enforcement.

If observability lets you see what happened, governance ensures that what happens follows rules.

In insurance, those rules may include:

- State-level regulatory requirements

- Internal underwriting guidelines

- Fairness and bias policies

- Privacy laws such as HIPAA

In banking, governance includes:

- Anti-money laundering requirements

- Fair lending laws

- Data protection regulations

Governance in AI means putting guardrails around the system so it cannot step outside approved boundaries.

In the diagram, governance appears in multiple forms: safety guardrails, compliance shields, and human oversight mechanisms.

Step 4: The RAG Triad – Groundedness, Context Relevance, Answer Relevance

Now we come to the RAG triad, which sounds complex but is simple when broken down.

When a system retrieves documents and generates an answer, three things must be evaluated:

Groundedness means: Is the answer actually supported by the retrieved documents? In other words, did the model invent anything?

Context relevance means: Were the retrieved documents actually relevant to the user’s question? If the wrong documents are retrieved, even a perfect model can produce a wrong answer.

Answer relevance means: Does the final answer actually address the original question?

If any one of these fails, the system becomes unreliable.

In insurance, imagine a claim decision based on the wrong policy version. In banking, imagine a credit decision based on outdated guidelines.

The triad ensures the system remains faithful to source documents and relevant to the question asked.

Step 5: What Is a Judge LLM?

This is an advanced but powerful idea.

A Judge LLM is a second model used to evaluate the output of the first model.

Think of it like peer review.

The primary model generates an answer using retrieved documents. Then, a separate model checks:

- Is the answer consistent with the source documents?

- Is it missing required disclosures?

- Is it violating any compliance policy?

If the answer passes validation, it is marked as approved. If it fails, it is flagged or blocked.

In highly regulated industries, this second layer dramatically reduces risk.

It is similar to how large financial institutions use independent risk review functions separate from front-line decision-making teams.

Step 6: Safety Guardrails

Safety guardrails are explicit controls that prevent misuse or non-compliant behavior.

Examples include:

Redacting PHI/PII If the system processes insurance claims, it may encounter protected health information. Guardrails ensure that sensitive identifiers are masked or handled properly.

Blocking off-topic queries If a claims system is asked unrelated or inappropriate questions, it should refuse to answer.

Preventing policy violations If the model attempts to generate advice outside approved business scope, it should be stopped.

Guardrails are not about limiting intelligence. They are about aligning the system with legal and ethical boundaries.

Step 7: Monitoring Layer

The monitoring layer aggregates performance metrics.

It answers questions like:

- How often are answers flagged?

- What percentage of responses fail groundedness checks?

- Are certain document sets causing retrieval errors?

- Is the model drifting over time?

Monitoring turns AI from a static deployment into a continuously managed system.

In insurance or banking, this is critical. Regulators expect ongoing oversight, not one-time validation.

Step 8: Audit Trails and Compliance

The audit trail connects everything.

Every interaction is logged with:

- Unique trace ID

- Retrieved documents

- Generated output

- Validation results

- Guardrail triggers

This enables forensic reconstruction.

If a customer disputes a decision, the organization can demonstrate:

- Which documents were used

- How the answer was formed

- Whether policy controls were enforced

That level of transparency builds regulatory trust.

So What Is This All About?

At a high level, the image is describing how to make AI production-grade for regulated industries.

It is not about experimentation.

It is about industrial-strength AI systems that are:

Observable Governed Auditable Safe Compliant

Without these layers, AI remains a demo. With them, AI becomes infrastructure.

Why This Matters for Insurance, Banking, and Property & Casualty

In insurance—especially Property & Casualty—decisions affect coverage, claims payments, litigation exposure, and regulatory scrutiny. Every decision must be defensible.

In banking, AI may influence credit decisions, fraud alerts, or compliance reviews. Mistakes can lead to fines or reputational damage.

In healthcare insurance, incorrect handling of PHI can result in legal penalties.

In all these domains, the cost of an AI hallucination is not embarrassment. It is financial, legal, and reputational risk.

Observability and governance frameworks transform AI from a creative engine into a controlled decision-support system.

They ensure that:

- AI decisions are grounded in approved documents

- Sensitive data is protected

- Human oversight is preserved

- Every action is traceable

Final Thought

The future of AI in regulated industries will not be determined by model size.

It will be determined by control systems.

The organizations that succeed will not simply deploy language models. They will build observability layers, governance frameworks, validation mechanisms, and audit trails around them.

That is what this diagram represents.

It is not complexity for complexity’s sake. It is the blueprint for trustworthy AI in insurance, banking, and beyond.

When AI becomes accountable, explainable, and compliant, it stops being a novelty.

It becomes enterprise infrastructure.

If you are exploring how to implement compliant, observability and governance within your insurance workflows, I would welcome the opportunity to speak with you. Feel free to reach out directly at [email protected] or call me to discuss your specific use case and how this approach can be tailored to your organization’s operational and regulatory requirements.